Canadian Occupational Projection System (COPS)

Industrial Summary

Computer, Electronic and Electrical Products

NAICS 3341-3346; 3351-3359

This industry comprises establishments primarily engaged in manufacturing information and communications technology (ICT) devices, such as computers and peripherals, telecommunication and audio-video equipment, navigational and measuring instruments, as well as electronic components for such products. It also comprises establishments involved in manufacturing products that generate, distribute and use electrical power, such as generators, transformers, switchgears, batteries, wires, electrical motors and household appliances. ICT is the most important of the two segments, accounting for about two-thirds of production in 2021. Overall, the industry is highly export intensive, with about 75% of its revenues coming from abroad, largely from the United States which accounts for 70% of exports. The industry is also largely exposed to import penetration with a substantial share of domestic demand met by imports, mainly from the United States, China and Mexico. It employed 106,700 workers in 2021 (6.1% of total manufacturing employment), with 60% in the ICT segment. Employment is mostly concentrated in Ontario (53%) and Quebec (26%), and the workforce is predominantly composed of men (72%). Key occupations (4-digit NOC) include:[1]

- Electronics assemblers, fabricators, inspectors and testers (9523)

- Assemblers and inspectors, electrical appliance, apparatus and equipment manufacturing (9524)

- Electrical and electronics engineers (2133)

- Supervisors, electronics manufacturing (9222)

- Supervisors, electrical products manufacturing (9223)

- Machine operators and inspectors, electrical apparatus manufacturing (9527)

- Computer programmers and interactive media developers (2174)

- Electrical and electronics engineering technologists and technicians (2241)

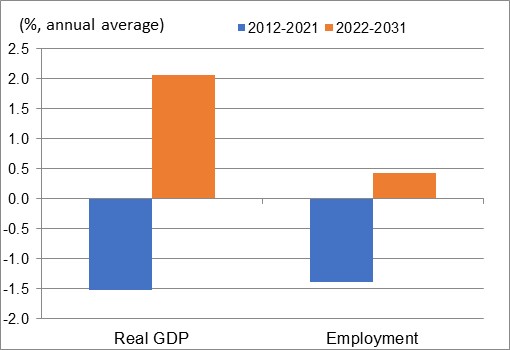

While the industry posted impressive growth in the late 1990s, largely driven by the strong performance of the ICT segment, production and employment fell almost continuously after the dot-com bubble burst of 2001. This reflects various challenges faced by the industry during that period, including the market saturation for ICT products in the early 2000s (largely due to an over capacity in the telecommunications infrastructure); the global recession of 2008-2009; the strong appreciation of the Canadian dollar (prior to 2014); and most importantly, the intensification of international competition on both domestic and foreign markets. Canada’s market share in the United States has been declining since the early 2000s, while imports from China have more than doubled in the last ten years. Producers are increasingly relocating to low-cost countries and China’s market share in Canada has been exceeding that of the United States since 2010 and is now accounting for more than 40% of Canadian imports of ICT products. Sales from the wireless communications segment were particularly affected by BlackBerry’s difficulties and decision to stop making phones, in part because of intense competition from Apple’s iPhone and Google’s Android supported devices. After reaching a through in 2014, the industry’s production rebounded from 2015 and 2019, primarily reflecting increased demand for semiconductors and other electronic components and growing exports to the United Sates, most likely attributable to a weaker Canadian dollar. Unsurprisingly, major shutdowns at the onset of the COVID-19 pandemic led to a sharp decline in production in 2020, offsetting all the increase recorded in the previous five years. And the modest rebound recorded in 2021 left the output significantly below its pre-pandemic level of 2019. On average, real GDP in the industry contracted at an annual rate of 1.5% over the period 2012-2021, compared to a decline of 1.4% for employment, with most of the job losses concentrated in 2013 and 2019. In contrast with many other industries, employment slightly increased in 2020-2021, most likely reflecting increased labour demand for the production of medical instruments. Productivity growth has been minimal over the past decade, averaging only 0.1% annually.

Over the period 2022-2031, output growth in computer, electronic and electrical products is projected to return to positive territory and strengthen markedly, with a significant part of the growth occurring in the short term as the industry continues to recover from the pandemic. In the longer term, the industry will continue to benefit from steady increases in business investment in North America and growing opportunities brought by new technologies. After posting negative growth over the past decade, business investment in machinery and equipment (M&E) is expected to straighten markedly in Canada and continue to grow at a solid pace in the United States, boosting domestic and foreign demand for ICT products which rely heavily on corporate spending. High replacement rates and perpetual innovation for many ICT products are also expected to keep driving consumer interest in new products. New technologies, such as mobile and cloud computing, the Internet of Things (IoT), 5G network, advanced robotics, machine learning and artificial intelligence, are projected to result in growing global demand for ICT products. With electronics being increasingly embedded in a variety of consumer products, such as vehicles and appliances, and considering the proliferation of applications for smartphones and other ICT devices, the design and manufacture of sensors, measuring, control and navigational instruments represent a key source of growth for the industry.

The need to reduce carbon emissions is also expected to drive the demand for greener, more energy-efficient buildings. Smart building automation systems rely on computer and electronics manufacturers to provide the various instruments and devices that can regulate and control buildings’ lighting, heating, ventilation and air conditioning. Canada has fared well in this market segment over the past several years, especially in the United States, as its competitiveness was boosted by innovative products that stand out relative to those of other competing nations. Those developments, combined with the relatively low value of the Canadian dollar and the Canada-U.S.-Mexico Agreement (CUSMA) should continue to stimulate exports in the industry and attract foreign investment. The electrical segment of the industry is also expected to benefit from the growing popularity of electric vehicles, which, according to the International Energy Agency[2], is projected to grow from 15 million vehicles in 2021 to 226 million in 2030. However, developing and maintaining intellectual property is critical for the industry’s success, as it accounts for three-quarters of total investment in the industry. In light of numerous and promising opportunities, real GDP growth is projected to average 2.1% annually over the period 2022-2031. Renewed growth in production is expected to result in a modest rebound of 0.4% per year in employment, although most of the growth in output should come from faster gains in productivity resulting from increased automation within the industry and the shift toward higher value-added products. On average, productivity is expected to rise by 1.7% annually over the coming decade.

Real GDP and Employment Growth Rates in Computer, Electronic and Electrical Products

Sources: Statistics Canada (historical) and ESDC 2022 COPS industrial projections.

| Real GDP | Employment | |

|---|---|---|

| 2012-2021 | -1.5 | -1.4 |

| 2022-2031 | 2.1 | 0.4 |

Sources: Statistics Canada (historical) and ESDC 2022 COPS industrial projections.

[1]Key occupations for manufacturing industries in general also include: Manufacturing managers (0911); Construction millwrights and industrial mechanics (7311); Material handlers (7452); Shippers and receivers (1521); Transport truck drivers (7511); Industrial engineering and manufacturing technologists and technicians (2233); Industrial electricians (7242); and Industrial and manufacturing engineers (2141).Back to text.

[2]International Energy Agency, Global Electric Vehicles (EV) Outlook.Return to text.